Expat Asset Planning: Why You Need a Local Will (And Why One Is Never Enough)

Subscribe to our newsletter for the latest expatriate news, views & analysis.

Living the expat life is an incredible adventure. You’ve successfully navigated international visas, mastered a new culture, and perhaps even purchased property or built a business abroad. But amidst the excitement of global living, there is one critical item that frequently slips through the cracks: estate planning.

Many global nomads assume that a will drafted in their home country covers their assets worldwide. Unfortunately, international estate law is rarely that accommodating. If you haven’t addressed your assets under the local laws of your current jurisdiction, your estate could face massive legal hurdles.

Here is why a local will is non-negotiable for expats, and how to keep your global wealth bulletproof.

The Myth of the "Worldwide Will"

It is a common misconception that a single will can seamlessly dictate what happens to your property across different continents. While some countries recognise foreign wills under specific treaties (like the Hague Convention), the practical execution is often a bureaucratic nightmare.

When you pass away, your estate typically goes through a legal process called probate. A probate court in one country cannot easily execute deeds or seize bank accounts in another.

The Reality Check: If you own a home in Spain, a bank account in Singapore, and retirement funds in the US, expecting a single court to sort it all out is a recipe for multi-year delays, exorbitant legal fees, and immense stress for your loved ones.

Why You Need Multiple Wills

To protect your global wealth, international cross-border legal experts frequently recommend a strategy of multiple wills—specifically, one will for each country where you hold major assets.

Jurisdiction-Specific Clarity: A local will is written in the local language, adheres strictly to local legal templates, and names executors who can physically operate within that country.

Faster Probate: Instead of waiting for a foreign court to validate your home-country will and translate it, local courts can process a local will immediately.

Asset Isolation: If a dispute arises over your assets in one country, it won't necessarily freeze your assets in another.

The "Forced Heirship" Trap

If you think your assets will automatically go to whomever you choose, you might be in for a surprise. Many regions - particularly in Europe, Latin America, and the Middle East - operate under forced heirship laws.

Unlike common law countries (like the US or the UK), where you have testamentary freedom to leave your estate to anyone, civil law and Sharia law jurisdictions have strict rules about asset distribution.

Mandatory Percentages

Local laws may mandate that a specific percentage of your estate must go to your spouse, children, or parents, entirely overriding whatever you wrote in your home-country will.

The Expat Loophole (Sometimes)

Some regions, like the European Union (under the EU Succession Regulation No. 650/2012), allow expats to choose the law of their nationality to govern their estate instead of the local law. However, you must explicitly declare this choice in a legally binding local document.

How to Properly Structure Your Estate

To ensure your estate planning is legally bulletproof, you must change how you frame your asset protection. Don't look for one document to rule them all. Instead, take a localised approach:

Step 1: Map Your Global Footprint

Inventory every major asset you own and categorise them by jurisdiction. This includes real estate, corporate entities, bank accounts, investments, and valuable physical property.

Step 2: Craft Separate, Coordinated Wills

Work with estate attorneys in each relevant jurisdiction to draft separate wills.

Crucial Warning

Ensure that a new local will does not accidentally contain a standard revocation clause that invalidates all previous wills. Your lawyers must explicitly state that each will only applies to assets within that specific country.

Step 3: Align with Local Tax Laws

Inheritance tax structures vary wildly across the globe. What is tax-free in your home country might be taxed at 40% in your country of residence. Local estate planning ensures your wealth isn't unnecessarily eaten away by foreign probate taxes.

The Bottom Line

When you are a global nomad, your estate planning must be as international as your lifestyle. Securing a local will in the jurisdiction where your assets reside isn't just a safety measure - it is the only way to ensure your legacy is protected and your family is looked after, no matter where in the world you call home.

Take Action: Protect Your Worldwide Assets

Whether you have a UK pension plan worth £1 million (which carries a potential £400,000 inheritance tax liability) or an overseas villa worth £500,000, your hard-earned wealth is vulnerable to the global reach of the taxman.

Planning "a good way to die" isn't something that should be morbid… it is an act of financial wisdom to protect the people you leave behind from legal chaos and financial ruin.

We brings almost 25 years of expert cross-border experience, helping families transition seamlessly from the UK to international lives.

Contact the team today to book your free review and discover the right combination of wills, trusts, and lifetime structures to safeguard your legacy.

Residex

Residex helps you track, assess and plan your tax residency with clarity, evidence & confidence.

Need help & guidance?

Contact us or book a free review with one of our expat experts today.

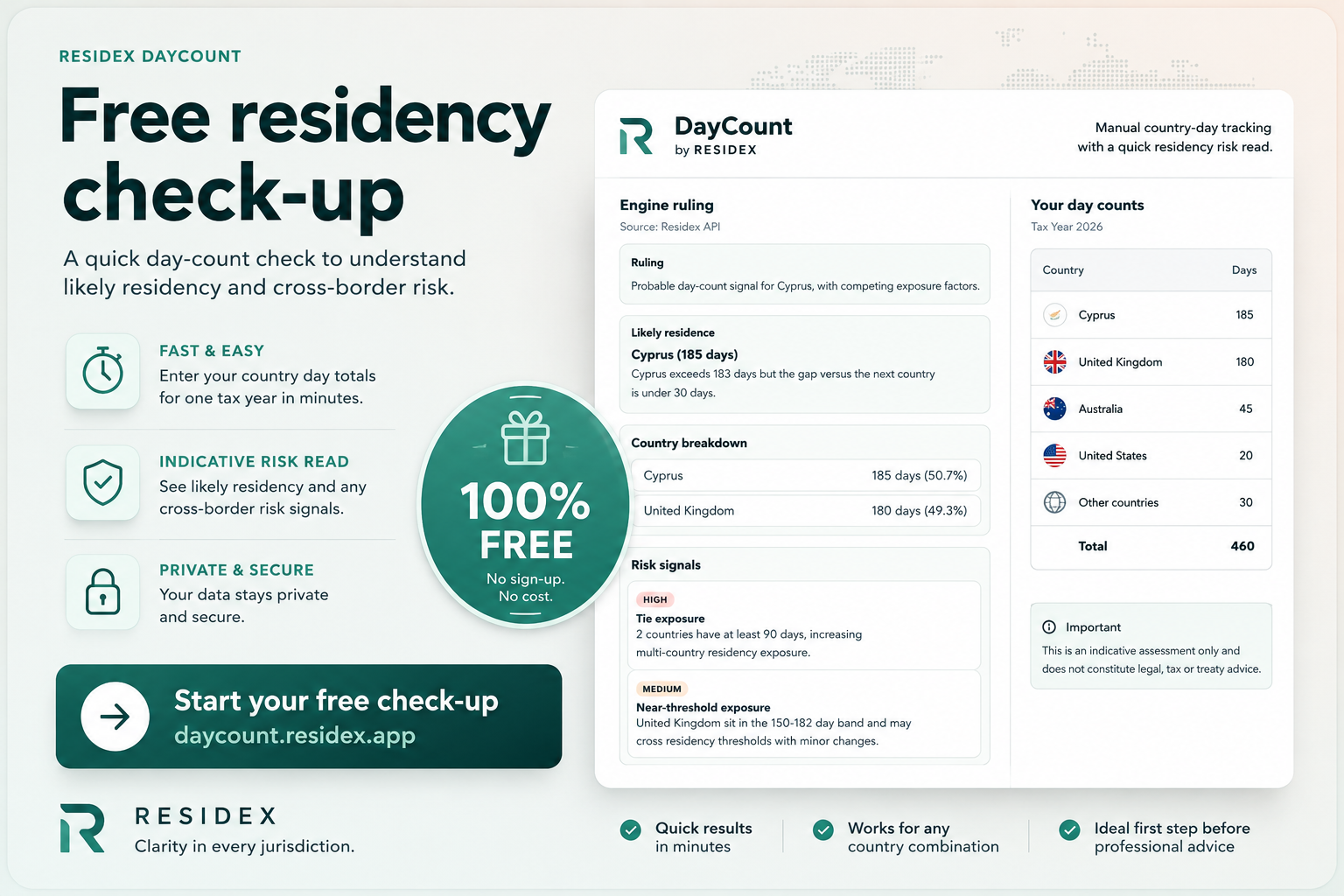

Get your free residency risk assessment.

We developed DayCount to allow you to enter the days you spend in a country and get a free quick residency risk assesment.