A Good Way to Die: The UK Expat’s Guide to Cross-Border Estate Planning

Subscribe to our newsletter for the latest expatriate news, views & analysis.

Moving abroad brings sun, adventure, and new opportunities but it also brings a tangled web of cross-border tax and legal liabilities.

As part of the ongoing series, "A Good Way to Die," this article will break down exactly how the global reach of the UK’s Her Majesty's Revenue and Customs (HMRC) can catch expats off guard, and what you can do to protect your family, property, and business assets.

If you own assets in the UK and live in the EU (or vice versa), here is what you need to know to protect your estate down the generations.

The Sticky Trap of UK Domicile Status

Many British expats assume that living outside the UK for years automatically shields them from the UK tax net. This is a dangerous misconception.

While you can change your residency relatively easily, your domicile is incredibly sticky. As an individual born in the UK, you will almost always remain UK-domiciled in the eyes of HMRC. Even if you live abroad for 20 years and establish a new life, spending just one day back in the UK - or merely demonstrating an intent to return eventually - can deem you UK-domiciled for inheritance tax purposes.

Why does this matter? If you are deemed UK-domiciled at the time of your death, the UK claims a 40% Inheritance Tax (IHT) on your worldwide assets, not just your UK-based ones.

The Cost of Doing Nothing

To illustrate the heavy burden of UK taxation, look at the potential liabilities an expat faces without proactive planning:

| Tax Type | UK Expat Liability Rate |

|---|---|

| Property Rental Income Tax | Up to 47% |

| Income Tax | Up to 45% |

| Dividend Tax | Up to 39% |

| Corporation Tax | Up to 25% |

| Capital Gains Tax (CGT) | Up to 24% |

| Inheritance Tax (Dying) | 40% |

| Lifetime Gift / Trust Tax | 20% |

Navigating the EU Succession Maze

If you are legally resident and die in an EU country such as Cyprus, Greece, Spain, or Portugal then the laws of intestacy of that specific country apply to your estate by default.

This introduces two massive headaches for expats:

Forced Heirship Laws

In countries like Cyprus, strict "forced heirship" laws dictate exactly how your estate must be divided among your children and spouse. Under these local systems, you have very little discretionary freedom to distribute your assets as you please. If you have a complicated family structure - such as second marriages, stepchildren, or business partners—local laws can entirely disrupt your wishes.

Local Property Quirks

Every country defines and administers assets differently. For example, while a vehicle in the UK is treated as a personal chattel (and doesn't require complex administration), in Cyprus, a car is classified as real estate. This means your loved ones must go through formal probate administration just to transfer ownership of a vehicle, alongside personal bank accounts and company shares.

To override local forced heirship rules, expats living in the EU must draft a local will that explicitly declares they want their estate settled under the jurisdiction of their home country (e.g., English or Scottish law).

However, a word of caution: Tying your estate back to UK law can inadvertently signal to HMRC that you still consider the UK your permanent home, reinforcing your UK domicile status and triggering that 40% worldwide inheritance tax. It is a delicate tightrope that requires expert execution.

Beyond Wills: The Power of Cross-Border Trusts

While a properly drafted will is a necessary baseline, it still forces your estate into the standard probate process. Probate creates significant delays, triggers third-party legal fees, and requires tax clearances in every country where you hold fixed assets.

To bypass probate entirely, strategic expats turn to Lifetime Trusts.

When you place assets (like overseas property or investments) into a family or business trust, you no longer legally own them.. the trust does. However, you can retain a degree of control and enjoy the benefits of those assets during your lifetime.

The "Duke of Westminster" Strategy

Think of it like the Duke of Westminster, whose family represents one of the wealthiest portfolios in Britain, spanning vast areas of London. The Duke doesn't personally own those multi-billion-pound assets; he is a trustee of a family trust. The trust generates income and security for the family down the generations, completely insulated from massive inheritance tax hits.

Speed of Transfer

While international probate can take months or even years, administering and handing over a trust to new trustees and beneficiaries typically takes just two weeks.

Tax Mitigation

Properly structured lifetime gifts into a trust can remove assets from your taxable estate entirely, provided you avoid the "gift with reservation" traps.

Take Action: Protect Your Worldwide Assets

Whether you have a UK pension plan worth £1 million (which carries a potential £400,000 inheritance tax liability) or an overseas villa worth £500,000, your hard-earned wealth is vulnerable to the global reach of the taxman.

Planning "a good way to die" isn't morbid… it is an act of love and financial wisdom to protect the people you leave behind from legal chaos and financial ruin.

We brings almost 25 years of expert cross-border experience, helping families transition seamlessly from the UK to international lives.

Contact the team today to book your free review and discover the right combination of wills, trusts, and lifetime structures to safeguard your legacy.

Residex

Residex helps you track, assess and plan your tax residency with clarity, evidence & confidence.

Need help & guidance?

Contact us or book a free review with one of our expat experts today.

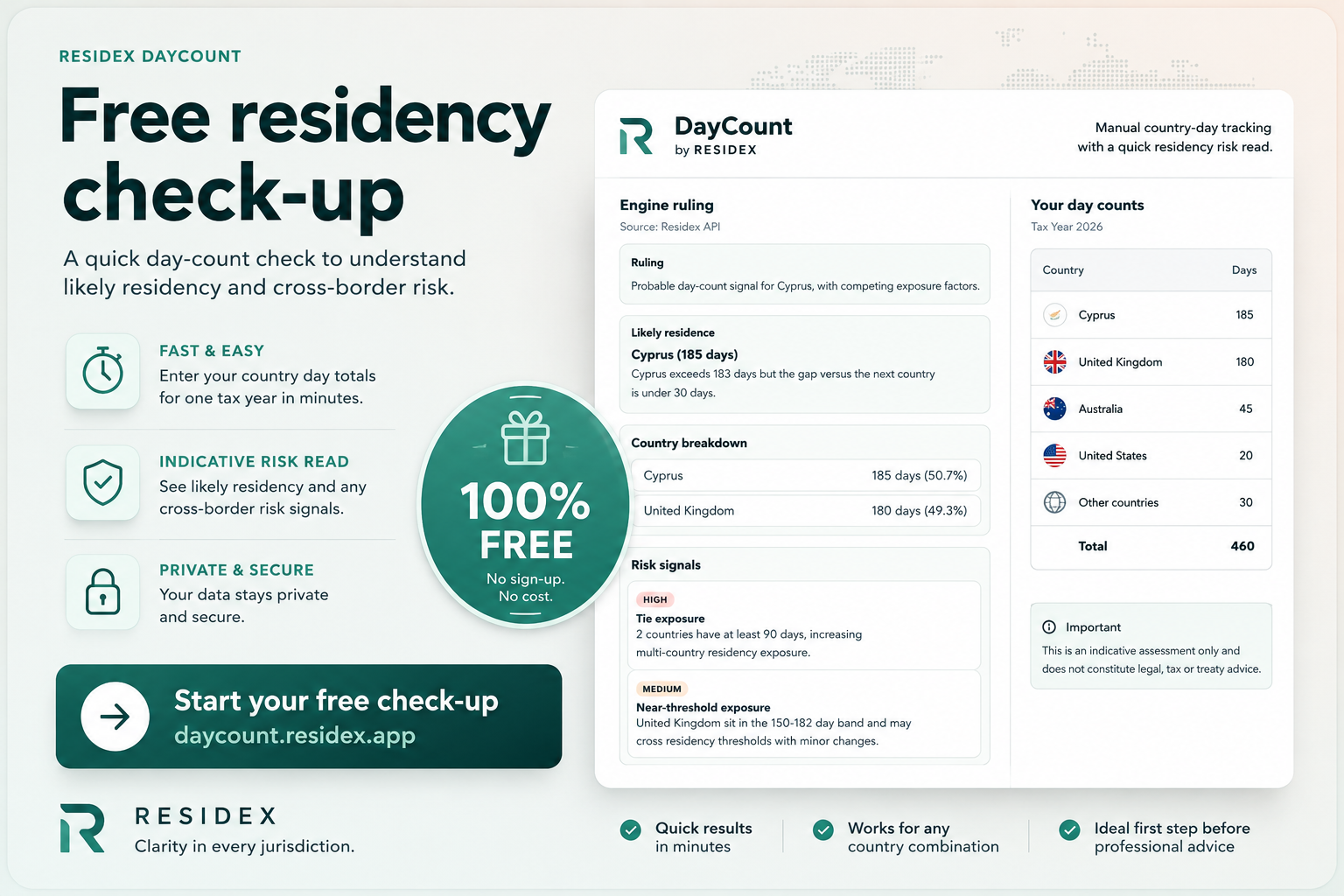

Get your free residency risk assessment.

We developed DayCount to allow you to enter the days you spend in a country and get a free quick residency risk assesment.