A Good Way to Die: How to Protect Your Family’s Wealth Across Generations

Subscribe to our newsletter for the latest expatriate news, views & analysis.

What does it mean to have "a good way to die"? It doesn’t mean your time is up today - in fact, the goal is to live a long, happy life to 100 and beyond. Instead, a good way to die is an philosophy of preparation. It means planning ahead so your estate is organised, your spouse and children are protected, and the administrative burden on your grieving family is entirely minimised.

Failing to plan means leaving behind a maze of costly probate delays, capital gains taxes, legal fees, and overseas asset complications. Fortunately, you can take control of your legacy today.

The Changing Landscape of UK Inheritance Tax

For over a decade, the UK inheritance tax (IHT) personal allowance has been frozen at £325,000 per person. While the threshold has stood still, property values and investment portfolios have climbed higher and higher. The result? More everyday families are being dragged into the 40% tax bracket.

To complicate matters, the government has added pension pots to the inheritance tax pool. Previously, a spouse or child could inherit a pension fund largely free of IHT. Now, that pot faces the same 40% hit. It's a massive win for the taxman, but a devastating loss for your family's financial security.

High-Risk vs. Low-Risk Mitigation

When looking for ways to protect wealth, some high-net-worth individuals turn to aggressive strategies, such as creating private unlimited companies to discreetly gift assets.

A Word of Caution: Avoid high-risk schemes. Attempting to gift your entire estate away rapidly can trigger a lifetime 20% inheritance tax liability or lock you into stringent 7-year waiting periods. The government deliberately makes it difficult to divest your assets at the eleventh hour.

The Secret to Generational Wealth: "Own Nothing, Control Everything"

Look at the wealthiest structures in the world. The Rolex Corporation is run by a not-for-profit trust. Similarly, the Duke of Westminster is famously known as one of the richest men in Britain, but legally, he isn't. He is the beneficiary and trustee of a massive family trust that has preserved wealth from generation to generation since the days of his ancestors.

The core philosophy is simple: If you don’t legally own anything when you die, no probate is required, and no inheritance tax can be assessed.

By establishing a family or business trust to hold your shares, properties, and global investments, you ensure continuity. The trust doesn't die when you do.

Zero Probate Delays: While standard probate can take months or years, assets held in a trust can typically be handed over to new trustees within two weeks of receiving a death certificate.

Asset Enjoyment: You and your family can still live in the properties, drive the classic cars, and enjoy the dividend income generated by the assets held within the trust.

The Cyprus Advantage for Expats and Investors

You don’t have to live in Cyprus to take advantage of its powerful financial structures. Because Cyprus law is rooted in English common law, its international trust frameworks are robust, highly flexible, and recognized worldwide.

1. Zero Trust Taxes

For an international trust holding overseas assets, Cyprus levies no inheritance tax and no capital gains tax. While you cannot avoid localized taxes on UK rental income or immediate UK property sales, future growth built up within the trust is shielded.

2. Corporate Tax Optimisation

If your business trust is managed out of Cyprus, you can take advantage of a 15% corporation tax rate… a significant savings compared to the UK. You can retain your profits in the overseas company and eliminate further tax liabilities down the line.

3. The 5% Pension Strategy

If you want to rescue a large pension pot from the UK's 40% IHT trap, withdrawing it as a UK resident can trigger income tax rates up to 45%.

However, by relocating and becoming a tax resident of Cyprus, the rules change entirely. As a Cyprus resident, you can draw down your UK pension at a flat rate of just 5% tax, regardless of whether the pot is £1 million or £50 million. Once that cash is safely in your hands at a fraction of the tax cost, you can immediately gift it, place it into a family trust, and secure it for the next 200 years.

Take Action Before It's Too Late

Doing nothing is not a strategy. Waiting until ill health or old age forces your hand leaves your family vulnerable. While writing a will is an excellent first step, a business or family trust provides a bulletproof legacy.

At ProACT Partnership, we are passionate about protecting your wealth, your property, and your family from the costs and delays of probate. We offer a free review to help you look outside the box, evaluate your assets, and map out your global options.

Don't leave your family's future to chance. Contact us for help & guidance.

Need help & guidance?

Contact us or book a free review with one of our expat experts today.

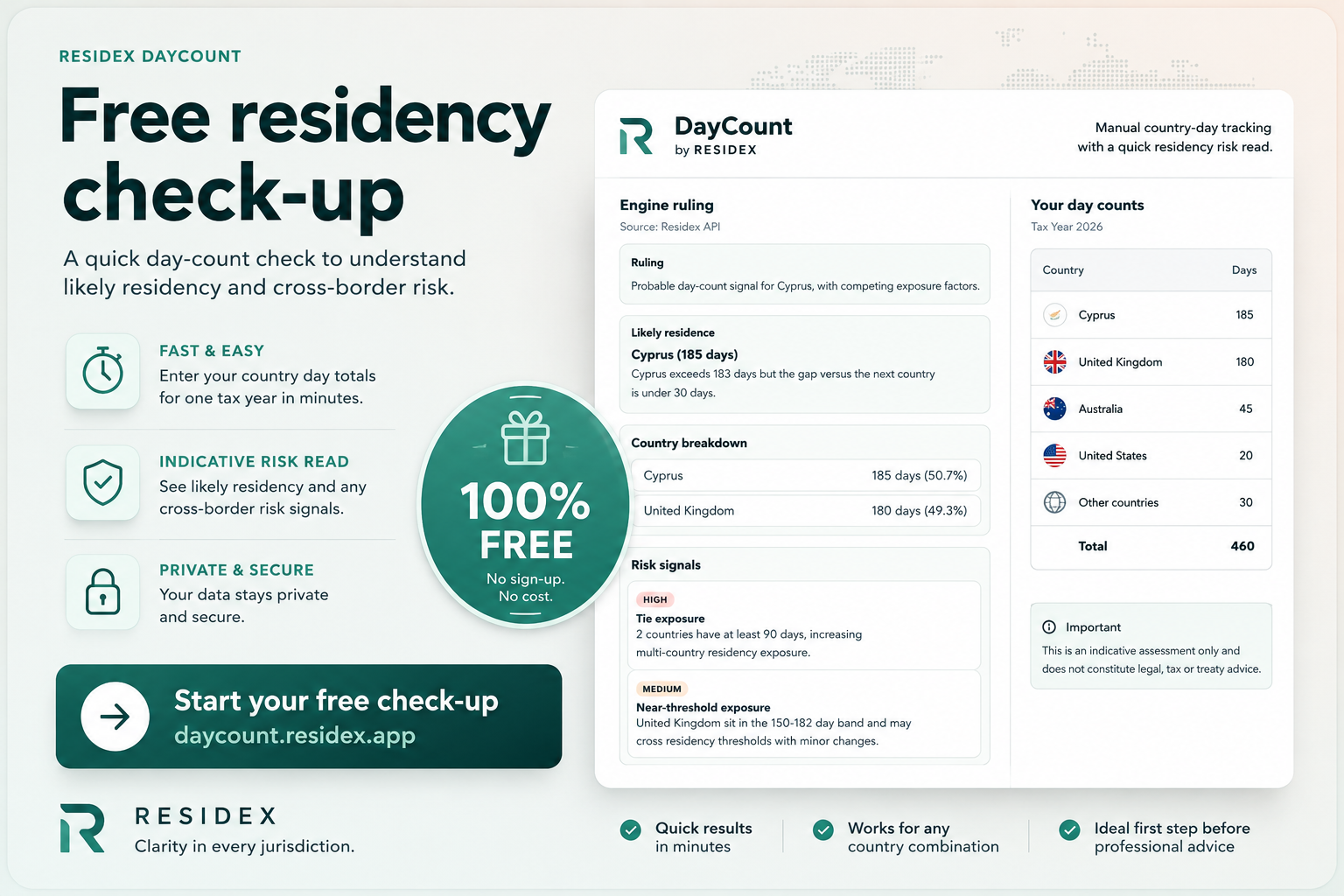

Get your free residency risk assessment.

We developed DayCount to allow you to enter the days you spend in a country and get a free quick residency risk assesment.